Navigating the complex world of vehicle protection requires a clear understanding of where personal boundaries end and professional liabilities begin. As we move into 2026, the distinction between personal auto insurance and commercial auto insurance has become more critical than ever. With the rise of the gig economy, remote work, and specialized business services, many drivers find themselves in a grey area where a single accident could lead to financial ruin if the wrong policy is in place. This comprehensive guide explores every facet of these two insurance types, providing you with the data and insights needed to protect your assets effectively.

- Defining the Foundation: What is Personal Auto Insurance?

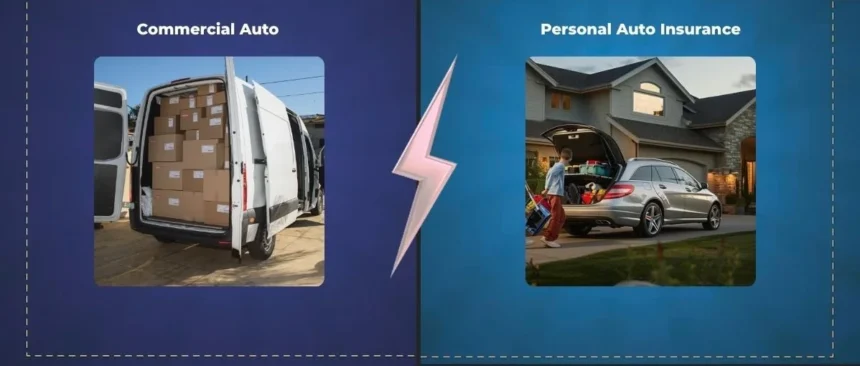

- Understanding the Scope: What is Commercial Auto Insurance?

- Key Differences at a Glance

- The Cost of Protection: 2025 and 2026 Market Trends

- The Grey Area: Business Use of Personal Vehicles

- Why Personal Policies Deny Business Claims

- 2026 Industry Trends: Technology and ESG

- How to Determine Which Policy You Need

- Steps to Choosing the Best Policy in 2026

- Evaluate Your Risk Profile

- Compare Quotes from Multiple Carriers

- Review Endorsements and Add-ons

- Consult with an Independent Agent

- Summary of Costs and Coverage (2025-2026 Data)

- Frequently Asked Questions

- Can I just use a personal policy if I am an independent contractor?

- Is commercial auto insurance tax-deductible?

- What happens if I use my business truck for a personal trip?

- Why is commercial insurance sometimes cheaper than personal?

- Final Thoughts for 2026

Defining the Foundation: What is Personal Auto Insurance?

Personal auto insurance is designed for the everyday driver. It provides coverage for individuals and families using their vehicles for personal activities. These activities typically include commuting to a single place of work, running errands, visiting friends, and going on road trips.

A standard personal policy focuses on protecting the driver, the passengers, and the vehicle itself against risks like collisions, theft, and natural disasters. Because the risk profile of an individual driver is generally lower than that of a business entity, these policies are usually more affordable. As of late 2025, the average annual premium for a full coverage personal policy in the United States is approximately $2,697, or about $225 per month.

Common Coverages in Personal Policies

Personal policies generally include a combination of the following components:

- Liability Coverage: Pays for bodily injury and property damage to others if you are at fault in an accident.

- Collision Coverage: Repairs or replaces your car if it is damaged in a crash.

- Comprehensive Coverage: Protects against non-collision events like fire, vandalism, or falling objects.

- Medical Payments or Personal Injury Protection (PIP): Covers medical expenses for you and your passengers regardless of fault.

- Uninsured and Underinsured Motorist Coverage: Protects you if the other driver lacks sufficient insurance.

Understanding the Scope: What is Commercial Auto Insurance?

Commercial auto insurance is a specialized product built for the unique risks associated with business operations. It is not just about who owns the vehicle, but how the vehicle is used. If a car, van, or truck is used to transport goods, deliver services, or carry passengers for a fee, it typically falls under the commercial category.

Business-use vehicles are often on the road more frequently and for longer durations than personal vehicles. They may also carry expensive equipment or hazardous materials, which significantly increases the liability exposure. Consequently, commercial policies offer much higher liability limits, often reaching $1 million or more, compared to the $100,000 to $300,000 limits common in personal insurance.

Specialized Coverages for Businesses

In addition to standard liability and physical damage, commercial policies offer specialized protections such as:

- Hired and Non-Owned Auto Insurance (HNOA): This is a vital endorsement for businesses that use vehicles they do not own, such as employee cars used for work errands.

- Cargo Insurance: Protects the goods being transported.

- Loading and Unloading Coverage: Covers damage that occurs while moving items into or out of the vehicle.

- Fleet Coverage: Allows a business to insure multiple vehicles under a single policy for easier management.

Key Differences at a Glance

Choosing the right policy depends on understanding the fundamental gaps between these two types of coverage.

Ownership and Eligibility

Personal insurance is issued to individuals. The policyholder is typically the owner of the vehicle and the primary driver. In contrast, commercial insurance is issued to a legal business entity or a sole proprietor. It can cover multiple drivers, including employees with varying driving records.

Coverage Limits and Risk Profiles

The financial stakes are higher in the business world. A business can be sued for millions of dollars if an employee causes a major accident. Personal insurance limits are often insufficient to cover these types of legal judgments. Commercial insurance is structured to provide a robust safety net that protects the business assets from being seized during a lawsuit.

Vehicle Types and Modifications

Personal policies are restricted to passenger vehicles like sedans, SUVs, and light trucks. Once a vehicle is modified for business use, such as adding a hydraulic lift, a permanent tool rack, or heavy duty towing equipment, it almost always requires a commercial policy. Semi-trucks, box trucks, and large passenger vans are exclusively covered by commercial insurance.

The Cost of Protection: 2025 and 2026 Market Trends

The insurance landscape is currently experiencing significant shifts. As we conclude 2025, premiums are being influenced by “social inflation,” which refers to the rising costs of legal settlements and jury awards.

Personal Insurance Costs

Personal rates have seen a steady climb of about 12 percent over the past year. Factors such as the high cost of auto parts and the increasing complexity of vehicle technology contribute to this rise. Drivers in urban areas like New York or Los Angeles continue to pay some of the highest premiums in the country due to traffic density and litigation rates.

Commercial Insurance Costs

Commercial premiums are highly variable depending on the industry. A small consulting firm might pay around $147 per month for its vehicle coverage. However, a landscaping company or a construction firm with higher risk exposure might see monthly premiums between $180 and $250 per vehicle. For-hire trucking remains the most expensive sector, with annual premiums for heavy trucks often exceeding $10,000 per vehicle.

The Grey Area: Business Use of Personal Vehicles

One of the most common mistakes small business owners and gig workers make is assuming their personal policy covers them while they are working. This is a dangerous misconception.

Rideshare and Delivery Services

If you drive for platforms like Uber, Lyft, or DoorDash, your standard personal policy likely has a “business use exclusion.” This means that if you have an accident while the app is on, your personal insurer can deny the claim. While these platforms provide some coverage, there are often gaps during the period when you are waiting for a request. To solve this, many providers now offer “Rideshare Endorsements” as an add-on to personal policies, though high-volume drivers may still need a full commercial policy.

Running Errands for the Boss

If an employee uses their own car to pick up office supplies or meet a client and causes an accident, the employer could be held liable. This is where Hired and Non-Owned Auto Insurance (HNOA) becomes essential. HNOA provides liability protection for the business in these specific scenarios, acting as a secondary layer of defense after the employee’s personal limits are exhausted.

Why Personal Policies Deny Business Claims

Insurers calculate premiums based on risk. When you buy a personal policy, you are telling the company that the vehicle will be used for low-risk personal tasks. Business driving involves different variables:

- High Mileage: More time on the road equals a higher statistical probability of an accident.

- Diverse Locations: Business vehicles often travel to unfamiliar or high-traffic areas.

- Driver Variability: Personal policies usually cover specific household members. Commercial policies must account for various employees driving the same vehicle.

If an accident occurs during a business activity and you only have a personal policy, the insurer may determine that you misrepresented the use of the vehicle. This can lead to a denied claim and the immediate cancellation of your policy.

2026 Industry Trends: Technology and ESG

The future of auto insurance is being shaped by data and sustainability.

The Rise of Telematics

Both personal and commercial insurers are moving toward usage-based insurance (UBI). By using telematics devices or smartphone apps to track driving behavior, companies can offer hyper-personalized rates. Safe drivers who avoid hard braking and late-night driving can see significant discounts. In 2026, we expect more commercial fleets to adopt advanced AI-driven telematics that not only track safety but also optimize routes to reduce fuel consumption.

ESG and Green Incentives

Environmental, Social, and Governance (ESG) criteria are starting to impact premiums. Businesses that transition their fleets to electric vehicles (EVs) or demonstrate a commitment to sustainability may receive preferred pricing. Some insurers are now offering “green vehicle” discounts for personal drivers as well, encouraging the shift away from internal combustion engines.

Climate Resilience

With the increasing frequency of extreme weather events, insurers are using sophisticated GIS and aerial imagery to assess risk. This affects premiums for vehicles parked in areas prone to floods, wildfires, or hailstorms. For businesses, having a documented disaster recovery plan can help in securing more favorable terms during policy renewals.

How to Determine Which Policy You Need

If you are unsure which coverage is right for you, consider the following questions:

- Who owns the vehicle? If the vehicle is owned by a corporation or LLC, it must have a commercial policy.

- What is the primary use? If you are transporting products, people for a fee, or heavy equipment, you need commercial coverage.

- Who is driving? If multiple employees need to drive the vehicle, a commercial policy is the standard solution.

- What are the liability requirements? If your business contracts require you to have $1 million in liability coverage, a personal policy will not suffice.

Steps to Choosing the Best Policy in 2026

To ensure you are getting the best value and protection, follow these steps:

Evaluate Your Risk Profile

Start by auditing how your vehicles are actually used. Track mileage, the types of cargo carried, and who has access to the keys. Understanding your risk is the first step toward accurate coverage.

Compare Quotes from Multiple Carriers

Insurance rates vary significantly between providers. Use online comparison tools to get quotes from top carriers like Progressive, State Farm, GEICO, and Liberty Mutual. For commercial needs, look into specialized providers like The Hartford or Travelers, who have deep expertise in business risks.

Review Endorsements and Add-ons

Sometimes a standard policy isn’t enough. Look for endorsements that fit your specific needs, such as “Blanket Additional Insured” for contractors or “Roadside Assistance” for delivery vehicles.

Consult with an Independent Agent

An independent agent can provide unbiased advice and help you navigate the nuances of state-specific laws. They have access to multiple insurance markets and can often find niche policies that aren’t available to the general public.

Summary of Costs and Coverage (2025-2026 Data)

The following table provides a high-level comparison of the financial expectations for both types of insurance.

| Feature | Personal Auto Insurance | Commercial Auto Insurance |

| Average Monthly Cost (Full Coverage) | $225 | $147 to $1,000+ |

| Standard Liability Limits | $100k to $300k | $500k to $1M+ |

| Primary Policyholder | Individual/Family | Business Entity/Sole Proprietor |

| Covered Drivers | Named household members | Employees and authorized agents |

| Vehicle Types | Sedans, SUVs, Light Trucks | Vans, Box Trucks, Semis, Specialized |

| Use Case | Commuting, Errands, Travel | Delivery, Transport, On-site Work |

Frequently Asked Questions

Can I just use a personal policy if I am an independent contractor?

It depends on the nature of your work. If you are a consultant driving to occasional meetings, a personal policy with a business-use notation might work. However, if you are carrying tools to job sites or delivering goods, most insurers will require a commercial policy.

Is commercial auto insurance tax-deductible?

Yes, for most business owners, the premiums paid for commercial auto insurance are a deductible business expense. Personal insurance premiums are generally not deductible unless you can prove a specific percentage of business use, and even then, the rules are more restrictive.

What happens if I use my business truck for a personal trip?

Most commercial policies cover “personal use” of the business vehicle, but you should verify this with your agent. There may be specific exclusions if the vehicle is used for long-distance personal travel.

Why is commercial insurance sometimes cheaper than personal?

While commercial liability is more expensive, some small business “Business Auto” policies for light vehicles can be surprisingly affordable because business owners are often viewed as more responsible and less likely to drive for purely recreational (and high-risk) reasons.

Final Thoughts for 2026

As vehicle technology and business models continue to evolve, the line between personal and professional life will keep blurring. However, the insurance industry maintains a strict separation to manage risk effectively. Whether you are an individual driver or a growing business, the key to financial security is transparency with your insurer.

Ensuring you have the correct policy in place is not just a legal requirement in most states: it is a fundamental part of a sound financial strategy. By staying informed about 2026 trends and regularly reviewing your coverage, you can drive with confidence, knowing that your assets and your future are well-protected.