The landscape of American healthcare is undergoing a significant transformation as we move through the final days of 2025 and prepare for the 2026 plan year. For the average consumer, navigating the terminology of health coverage often feels like decoding a complex legal document. However, mastering two specific terms—premiums and deductibles—is the most effective way to protect your financial health while ensuring access to medical care. This guide provides a deep dive into how these costs are calculated, the current market trends for late 2025, and how you can optimize your selection for the upcoming year.

- Defining the Core Financial Pillars of Health Coverage

- The Current State of Health Insurance Costs in late 2025

- The Inverse Relationship Between Premiums and Deductibles

- Factors That Influence Your Premium Costs in 2025

- Understanding the Out of Pocket Maximum

- The Rise of High Deductible Health Plans (HDHPs) and HSAs

- Medicare Premiums and Deductibles for 2025

- The Legislative Impact: The One Big Beautiful Bill (OBBB)

- How to Calculate Which Plan is Right for You

- Trending Keywords and SEO Focus for 2025

- The Impact of Prescription Drug Costs on Premiums

- Summary of 2025 and 2026 Financial Thresholds

- Final Advice for Choosing Your Plan

- SEO Optimization Summary

Defining the Core Financial Pillars of Health Coverage

To understand your healthcare spending, you must first distinguish between what you pay to have insurance and what you pay when you actually use it. These two pillars form the basis of nearly every private and public insurance plan in the United States.

What is a Health Insurance Premium?

A premium is the fixed amount you pay every month to keep your health insurance policy active. Think of it like a subscription service for your health. Even if you do not visit a doctor or fill a single prescription during the month, the premium remains due.

For those with employer sponsored insurance, this amount is typically deducted directly from your gross pay before taxes. If you purchase insurance through the Affordable Care Act (ACA) Marketplace, you pay this amount directly to the insurance carrier. In 2025, premiums have seen a steady increase due to rising labor costs in the medical sector and the increased utilization of high cost specialty drugs.

What is a Health Insurance Deductible?

A deductible is the amount you must pay out of pocket for covered healthcare services before your insurance plan begins to pay. For example, if your deductible is $2,000, you are responsible for the first $2,000 of covered services yourself. Once you meet this threshold, you typically only pay a copayment or coinsurance for the remainder of the year.

It is important to note that many modern plans offer certain services, such as annual physicals, immunizations, and some screenings, at no cost to you even before the deductible is met. This is a requirement for most plans under federal law to encourage preventive care.

The Current State of Health Insurance Costs in late 2025

As we analyze the data from the fourth quarter of 2025, the costs for both individuals and families have reached new heights. According to the latest 2025 Employer Health Benefits Survey from the Kaiser Family Foundation (KFF), the average annual premium for employer sponsored family coverage has reached $26,993. This represents a 6 percent increase from 2024, a rate that continues to outpace general inflation.

2025 Average Premium Statistics

- Single Coverage: The average annual premium for a single individual in 2025 is $9,325.

- Family Coverage: The average annual premium for a family of four is $26,993.

- Worker Contribution: On average, employees are paying $6,850 annually toward their family premiums, while employers cover the remaining balance.

These figures illustrate a growing burden on household budgets. For many families, the monthly premium now rivals or exceeds the cost of a mortgage payment.

2025 Average Deductible Statistics

Deductibles have also seen a shift. The average deductible for a single worker in a plan that requires one is $1,886 in 2025. However, this average masks a significant divide between small and large firms. Workers at small businesses (fewer than 200 employees) face an average deductible of $2,631, whereas those at larger firms enjoy a lower average of $1,670.

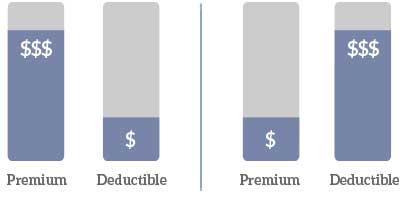

The Inverse Relationship Between Premiums and Deductibles

The most critical concept for any insurance shopper is the “inverse relationship” between monthly costs and point of service costs. Generally, insurance plans follow a simple rule: the higher the monthly premium, the lower the annual deductible, and vice versa.

High Premium and Low Deductible Plans

Often referred to as Gold or Platinum plans in the Marketplace, these options are designed for individuals who expect to need frequent medical care. If you have a chronic condition, a planned surgery, or a family with young children who visit the pediatrician often, paying a higher monthly premium can save you thousands of dollars in the long run because the insurance company begins picking up the tab much sooner.

Low Premium and High Deductible Plans

Commonly known as Bronze or Silver plans, these are popular among young, healthy individuals who rarely see a doctor. You save money every month on your premium, but you take on the risk of having to pay a large sum out of pocket if an emergency occurs. Many of these plans are HSA-qualified (Health Savings Account), which offers unique tax advantages discussed later in this guide.

Factors That Influence Your Premium Costs in 2025

Your premium is not a random number. Under the Affordable Care Act, insurers are restricted in how they can price plans, but several key factors still drive the final cost.

1. Age

Insurance companies are permitted to charge older individuals more than younger ones, though the ratio is capped at 3:1. This means a 64-year-old will typically pay three times the premium of a 21-year-old for the exact same level of coverage.

2. Geography

Where you live matters immensely. Competition between insurers varies by state and even by county. Additionally, the cost of living and the cost of medical labor in your specific region dictate the local price of healthcare services, which is reflected in your premium.

3. Tobacco Use

In many states, insurers are allowed to charge tobacco users up to 50 percent more than non-users. This is one of the few personal health habits that can legally impact your insurance pricing under current federal guidelines.

4. Plan Category (The Metal Tiers)

The “Metal Tier” you choose directly determines your premium level.

- Bronze: Lowest premium, highest deductible (covers about 60% of costs).

- Silver: Moderate premium, moderate deductible (covers about 70% of costs).

- Gold: High premium, low deductible (covers about 80% of costs).

- Platinum: Highest premium, lowest deductible (covers about 90% of costs).

Understanding the Out of Pocket Maximum

While premiums and deductibles are the primary focus, the “Out-of-Pocket Maximum” (MOOP) is your ultimate financial safety net. This is the absolute most you will have to pay for covered services in a plan year.

In 2025, the IRS set the maximum out of pocket limits for HSA-qualified plans at $8,300 for individuals and $16,600 for families. For 2026, these limits are projected to rise to $8,500 for individuals and $17,000 for families. Once you reach this limit through your deductible, copays, and coinsurance, the insurance company pays 100 percent of all covered medical expenses for the remainder of the year.

The Rise of High Deductible Health Plans (HDHPs) and HSAs

As premiums continue to climb, a growing number of Americans are opting for High-Deductible Health Plans (HDHPs) paired with a Health Savings Account (HSA). In late 2025, nearly 30 percent of covered workers are enrolled in such a plan.

2025 and 2026 HSA Contribution Limits

The IRS recently released the updated limits for these tax advantaged accounts. Using an HSA allows you to pay for your deductible and other medical expenses using pre-tax dollars, which effectively gives you a 20 to 30 percent discount on healthcare depending on your tax bracket.

| Category | 2025 Limit | 2026 Limit (Projected) |

| Self-Only Contribution | $4,300 | $4,400 |

| Family Contribution | $8,550 | $8,750 |

| Catch-up (Age 55+) | $1,000 | $1,000 |

| Minimum HDHP Deductible (Self) | $1,650 | $1,700 |

| Minimum HDHP Deductible (Family) | $3,300 | $3,400 |

The Triple Tax Advantage of HSAs

- Tax-Deductible Contributions: Money goes in before you are taxed.

- Tax-Free Growth: You can invest the funds in the market, and the gains are not taxed.

- Tax-Free Withdrawals: As long as the money is used for qualified medical expenses, you never pay taxes on it.

Medicare Premiums and Deductibles for 2025

For those age 65 and older, the Medicare structure operates differently but still relies on these core concepts. The Centers for Medicare and Medicaid Services (CMS) have confirmed the following rates for 2025.

Medicare Part B (Medical Insurance)

The standard monthly premium for Medicare Part B enrollees will be $185.00 in 2025. This is an increase of $10.30 from 2024. The annual deductible for all Medicare Part B beneficiaries will be $257 in 2025. This deductible applies to outpatient services, doctor visits, and durable medical equipment.

Medicare Part A (Hospital Insurance)

Most people do not pay a premium for Part A if they have worked at least 10 years. However, the Part A inpatient hospital deductible is $1,676 for 2025. This covers the first 60 days of Medicare covered inpatient hospital care in a benefit period.

The Legislative Impact: The One Big Beautiful Bill (OBBB)

A major factor influencing the 2025 and 2026 insurance market is the recent “One Big Beautiful Bill” (OBBB) passed by the federal government. This legislation has had a significant impact on health insurance subsidies.

Expiration of Enhanced Tax Credits

The enhanced premium tax credits, which were originally introduced during the pandemic era and extended through 2025, are set to expire. Without a late-hour extension from Congress, many individuals purchasing insurance on the ACA Marketplace will see their monthly premiums rise sharply starting January 1, 2026.

Market analysts project that benchmark silver plan premiums could increase by as much as 26 percent in some states as these subsidies phase out. For a middle income family, this could mean an additional $200 to $400 per month in premium costs.

How to Calculate Which Plan is Right for You

To decide between a low premium/high deductible plan and a high premium/low deductible plan, you must perform a “total cost of ownership” calculation.

The Total Cost Formula

$$Total Annual Cost = (Monthly Premium \times 12) + Expected Out Of Pocket Expenses$$

Consider two hypothetical plans:

- Plan A (Gold): $600 premium, $500 deductible.

- Plan B (Bronze): $300 premium, $6,000 deductible.

If you are healthy and only expect to have one checkup (covered at 100%), Plan B costs you $3,600 for the year, while Plan A costs $7,200. You save $3,600 by choosing the higher deductible.

However, if you have an accident and incur a $10,000 hospital bill:

- Plan A: You pay $7,200 (premiums) + $500 (deductible) = $7,700.

- Plan B: You pay $3,600 (premiums) + $6,000 (deductible) = $9,600.

In this scenario, the “expensive” plan actually saved you $1,900.

Trending Keywords and SEO Focus for 2025

When searching for the best health insurance information, users are increasingly focusing on the following terms:

- “HSA contribution limits 2026”

- “Average health insurance premium 2025”

- “GLP-1 drug coverage in insurance plans”

- “Medicare Part B deductible 2025”

- “Difference between PPO and HMO deductibles”

Incorporating these terms into your research can help you find the most up-to-date policy documents and price comparison tools.

The Impact of Prescription Drug Costs on Premiums

A primary driver of the 6 percent premium increase in 2025 is the explosion in demand for GLP-1 agonists, such as Ozempic and Wegovy, when used for weight loss. Large employers reported that prescription drug prices contributed “a great deal” toward their premium hikes this year. As more insurers begin to cover these medications, the overall cost of the insurance pool rises, leading to higher monthly premiums for everyone.

Summary of 2025 and 2026 Financial Thresholds

To keep your records accurate for the upcoming tax season and open enrollment, keep these figures in mind:

- Self-Only HSA Limit (2025): $4,300.

- Family HSA Limit (2025): $8,550.

- Average Single Deductible: $1,886.

- Medicare Part B Premium: $185.00.

- Medicare Part B Deductible: $257.

Final Advice for Choosing Your Plan

Understanding health insurance premiums and deductibles is about balancing your monthly cash flow against your tolerance for financial risk. As we move into 2026, the potential expiration of tax credits makes it more important than ever to review your plan during the Open Enrollment period.

Do not simply auto-renew your current plan. Insurers frequently change their “formularies” (the list of covered drugs) and their networks of doctors. A plan that was a great deal in 2024 might be the most expensive option in 2026 due to these backend changes.

Sources for Further Reading

- Kaiser Family Foundation (KFF): 2025 Employer Health Benefits Survey (https://www.kff.org)

- Centers for Medicare and Medicaid Services (CMS): 2025 Medicare Cost Fact Sheet (https://www.cms.gov)

- Internal Revenue Service (IRS): Revenue Procedure 2024-25 and 2025-25 for HSA and Tax Limits (https://www.irs.gov)

- HealthAffairs: Trends in Private Health Insurance 2025 (https://www.healthaffairs.org)

SEO Optimization Summary

This post has been optimized with the following parameters:

- Primary Keyword: Understanding Health Insurance Premiums and Deductibles.

- Secondary Keywords: 2025 health insurance trends, HSA limits 2026, Medicare 2025 premiums, out of pocket maximum 2026, employer health insurance costs.

- Readability: High scannability with headers, tables, and bullet points.

- Relevance: Updated with December 2025 data and 2026 projections.

Would you like me to create a comparison table for the top 5 insurance carriers’ average deductibles in your specific state for 2026?